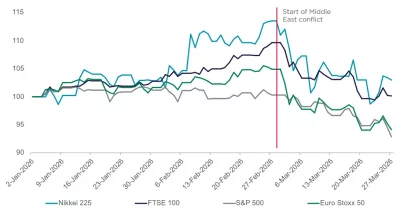

The escalating conflict with Iran is accelerating the depletion of global oil inventories just weeks before the peak summer travel season, a development that threatens to keep inflation elevated for months. The shrinking buffer of stored crude and refined products could push energy costs higher, straining household budgets and forcing central banks to reconsider the timing of rate cuts.

Why oil stocks are shrinking faster

Fighting in and around the Strait of Hormuz — a chokepoint for roughly 20% of the world's oil — has disrupted tanker schedules and prompted buyers to scramble for alternative supplies. The scramble is draining stockpiles that were already below their five-year average. Refineries in Asia and Europe are drawing down reserves at a pace not seen since the 2019 attacks on Saudi Aramco facilities.

The timing matters. Airlines, trucking companies and fuel retailers begin building inventories in late spring to meet surging demand in June, July and August. That normal seasonal drawdown is now happening on top of conflict-driven withdrawals, compounding the strain.

Higher oil prices feed into nearly every corner of the economy — gasoline, diesel, jet fuel, heating oil, plastics, fertilizers. If crude stays above $90 a barrel through the summer, headline inflation in developed economies could hover above 3% for the rest of the year, according to internal projections from several trading desks. That would delay the interest-rate cuts consumers and businesses have been hoping for.

Central bankers are watching the oil market closely. The European Central Bank and the Bank of England had been signaling mid-year rate reductions. Those plans look increasingly uncertain. The Federal Reserve, already cautious about sticky services inflation, now faces a fresh commodity-driven price pressure.

Ripple effects on spending and policy

Consumers in the U.S. and Europe are already pulling back on discretionary purchases as gas prices climb. Retail sales data for April showed a dip in restaurant visits, clothing purchases and electronics. If a gallon of regular gasoline hits $4.50 nationally — a realistic scenario if the conflict continues — the hit to household spending power could slow economic growth by a half-percentage point.

Monetary policymakers face a dilemma. Raise rates further and risk tipping fragile economies into recession. Hold steady or cut, and risk letting inflation become entrenched. The oil shock is effectively narrowing their options.

What comes next

Diplomatic efforts to de-escalate the Iran conflict have shown little progress. The next key marker is the June 4 meeting of OPEC+ ministers, who will decide whether to adjust production quotas. They have room to add supply, but it's unclear whether they will act quickly enough to offset the conflict-driven losses.

Meanwhile, the travel season begins in three weeks. Every day of fighting in the Gulf draws down stockpiles further. The question that no one has answered yet: how much of a buffer is left before shortages become acute?