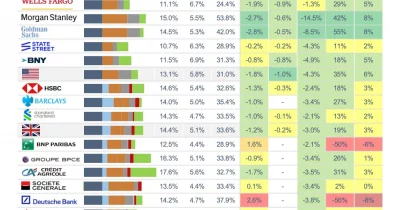

US and UK banks just got a massive boost in lending power. New deregulation of leverage ratios has freed up $1.3 trillion in additional capacity, according to financial authorities on both sides of the Atlantic. The move is expected to increase bank lending and revenue, but critics warn it could undermine financial stability and give traditional lenders an edge over emerging digital finance firms.

What the deregulation changes

Leverage ratios limit how much banks can lend relative to their capital. By loosening those requirements, regulators in the US and the UK effectively let banks take on more debt-funded lending without needing to raise extra equity. The $1.3 trillion figure represents the new room banks have to issue loans, buy bonds, or expand their balance sheets. That’s a lot of money – and it could flow into mortgages, corporate loans, and other credit markets.

The change doesn’t apply to all banks equally. Large institutions with complex balance sheets are likely to see the biggest benefit. Smaller lenders may still face tighter constraints. But overall, the industry is cheering the extra flexibility.

Why the shift now

Regulators in both countries argue that the old rules were too strict in a post-pandemic economy where credit demand is picking up. Banks had been complaining that leverage ratio constraints were holding back lending, especially for low-risk assets like government bonds. The new rules aim to put more capital to work without waiting for years of profit accumulation.

The deregulation also comes as digital finance competitors – fintechs, neobanks, and decentralized lenders – are eating into traditional banks’ market share. By giving banks more lending capacity, authorities hope to level the playing field. But that’s a double-edged sword.

Risks to financial stability

Critics inside and outside the regulatory community have raised alarms. More leverage means banks can absorb fewer losses before running into trouble. If a downturn hits, the extra $1.3 trillion in loans could turn into bad debts faster than banks can handle. The 2008 financial crisis was fueled by excessive leverage, and some worry this deregulation repeats old mistakes.

Central banks and finance ministries haven’t publicly detailed how they plan to monitor the increased risk. The new rules don’t come with new oversight tools, which leaves a gap. Banks will report their leverage ratios quarterly, but that may not be fast enough to catch trouble brewing.

Competition with digital finance

Digital finance firms operate under different rules. Many aren’t subject to leverage ratios at all. By boosting banks’ lending capacity, regulators are essentially tilting the field back toward traditional lenders. That could slow the growth of fintech lending, which had been gaining ground by offering faster, cheaper credit.

But it also raises a question: if banks can lend more, will they also invest in the technology needed to compete with digital-native startups? The deregulation doesn’t require them to upgrade their systems. Some may simply do more of the same, rather than innovate.

The next steps are unclear. Both the US and UK regulators have said they’ll monitor the effects, but no formal review timeline has been announced. Banks will likely start deploying the new capacity within the next quarter. Whether that leads to a lending boom or a stability headache is anyone’s guess – but the $1.3 trillion number ensures it won’t go unnoticed.